Table of Contents

Executive Summary

Gold remains a critical asset in the global financial system, serving both as a portfolio diversifier and a central bank reserve asset. Its value is primarily driven by real interest rates, inflation expectations, and geopolitical risk.

As the U.S. economy enters a late-cycle phase characterized by slowing growth, elevated geopolitical uncertainty, and potentially declining real interest rates, the macroeconomic environment is becoming increasingly supportive of gold.

What this means for investors

Gold should be viewed as a strategic allocation in portfolios, particularly as a hedge against macroeconomic uncertainty, inflation risk, and financial market volatility.

Macroeconomic Drivers of Gold

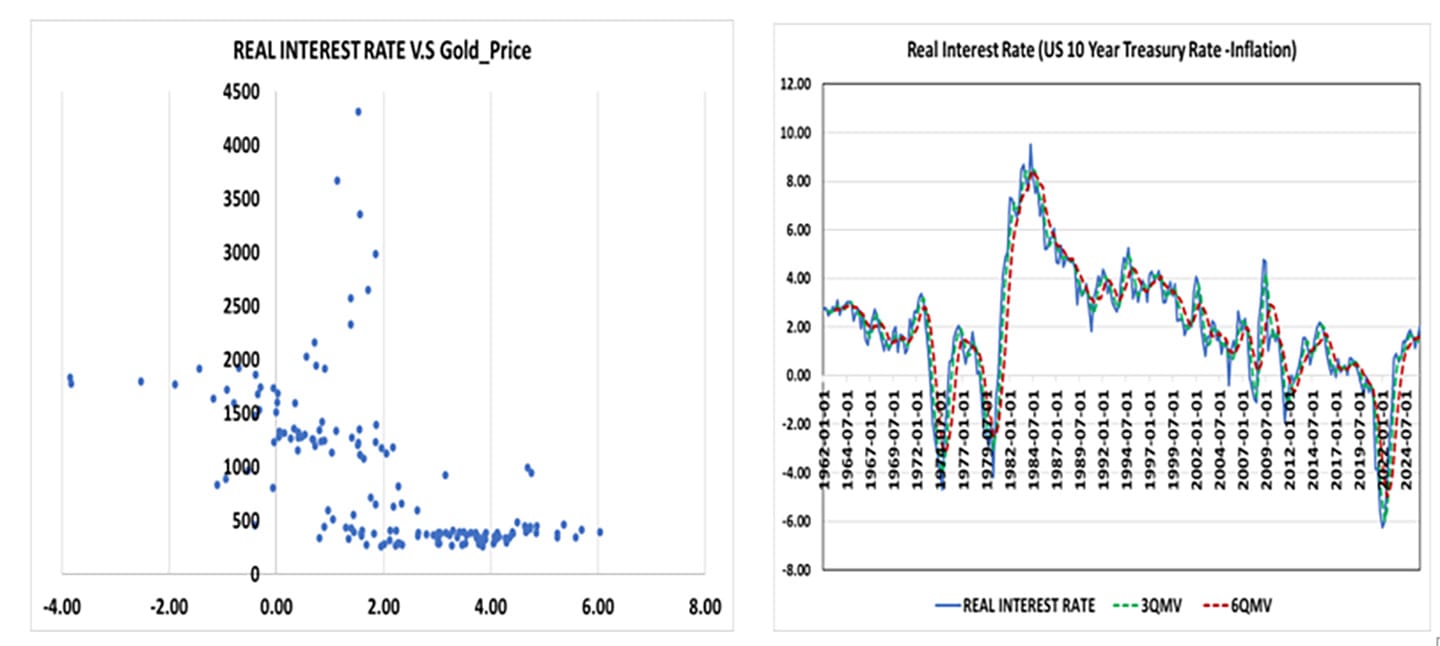

Real Interest Rates

Gold is fundamentally linked to real interest rates, which determine the opportunity cost of holding a non-yielding asset.

Rising real rates → negative for gold

Declining or negative real rates → supportive for gold

While the inverse relationship between gold and real interest rates is well established, it can weaken during periods of heightened uncertainty, when safe-haven demand becomes the dominant driver.

In general, higher real interest rates increase the opportunity cost of holding non-yielding assets, placing downward pressure on gold prices. Conversely, declining real rates reduce this opportunity cost, making gold more attractive and supporting higher prices.

The sharp decline in real interest rates during the COVID-19 period contributed to a significant increase in gold prices. More recently, expectations of rising real interest rates have exerted downward pressure on gold prices, contributing to the observed decline in early 2026.

Inflation Expectations

Gold acts as a store of value when inflation erodes real returns on financial assets.

Rising inflation expectations → increased demand for gold

Stagflationary environments → historically strong gold performance

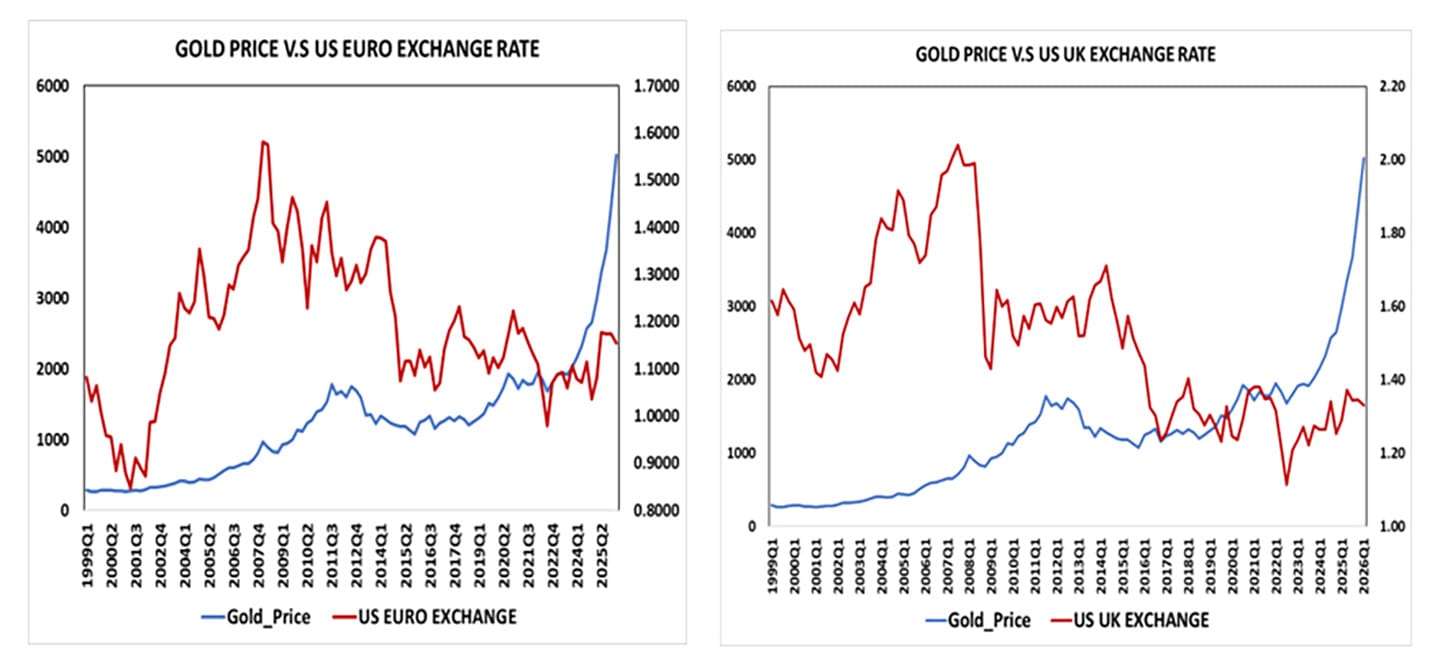

U.S. Dollar Dynamics

Gold exhibits a structural inverse relationship with the U.S. dollar.

USD strength → downward pressure on gold

USD weakness → supports gold demand globally

Geopolitical Risk and Financial Uncertainty

Gold serves as a defensive asset during periods of geopolitical and financial stress.

Elevated tensions—particularly in energy-sensitive regions—create upside risks to gold prices through higher inflation uncertainty and increased market volatility.

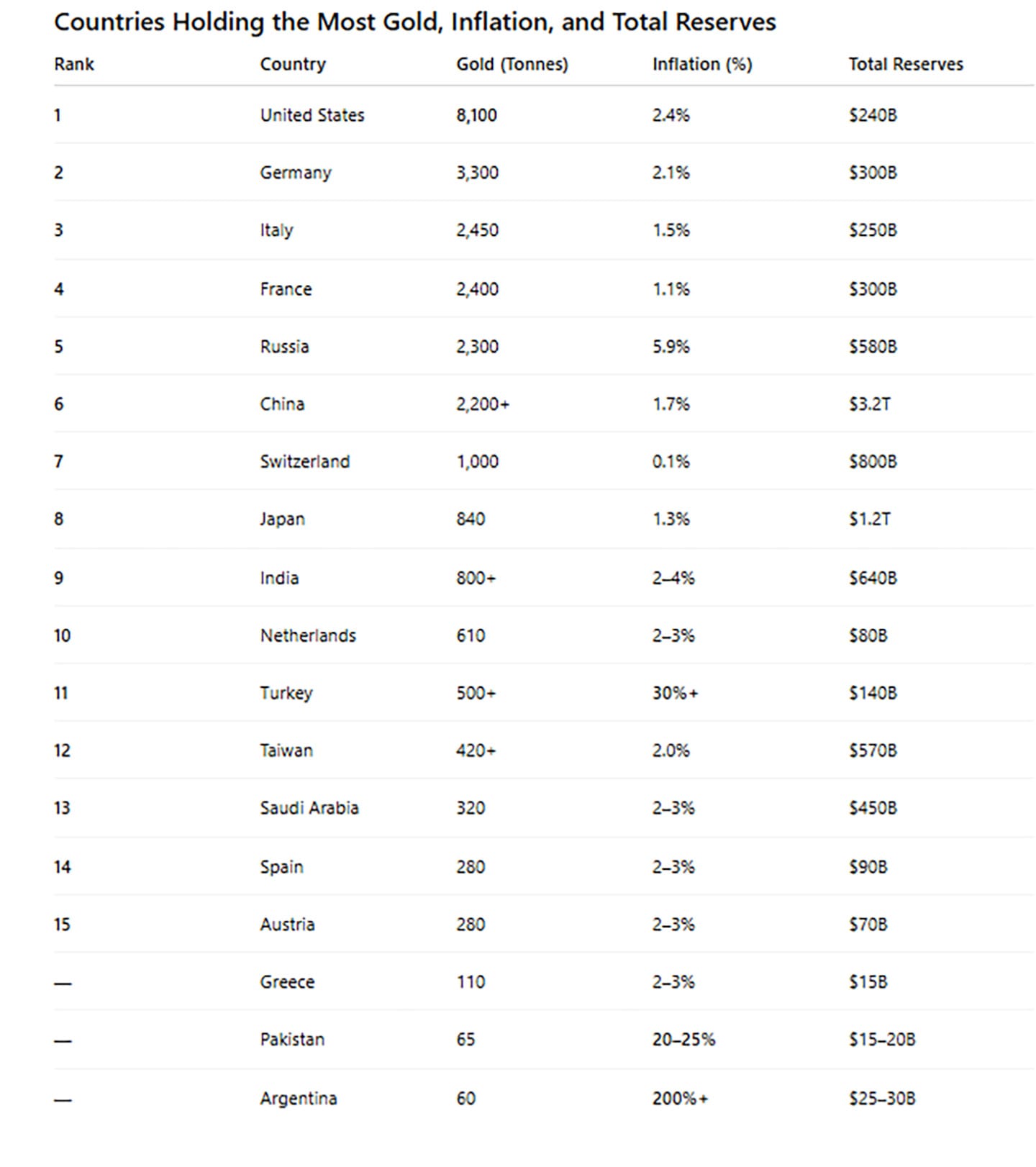

Gold as a Central Bank Reserve Asset

Gold remains a core component of global foreign exchange reserves, reflecting its role as a neutral store of value outside the fiat currency system. Central banks continue to accumulate gold to diversify reserves, mitigate currency risk, and strengthen financial credibility.

Sustained depreciation across major currencies reinforces gold’s role as a reserve asset. Over the past decade, both the euro and British pound have weakened significantly against the U.S. dollar, highlighting the structural vulnerability of fiat currencies. The euro declined by approximately 38% from 2008Q1 to 2022Q3, while the British pound fell by roughly 45% over a similar period. These trends underscore gold’s function as a durable store of value and a hedge against currency risk within global reserve portfolios.

Against this backdrop, central bank gold demand has risen—particularly among emerging markets—driven by efforts to reduce reliance on major reserve currencies and enhance balance sheet resilience.

Empirical Framework

Gold prices can be understood as a function of key macroeconomic variables:

Real interest rates

Inflation expectations

U.S. dollar strength

Financial market uncertainty

In simplified terms:

Gold Price = f (Real Interest Rates ↓, Inflation Expectations ↑, USD ↓, Risk ↑)

This framework highlights that gold is not driven by a single factor, but by the interaction of monetary policy, macroeconomic conditions, and global risk dynamics.

Outlook for Gold (2026–2027)

Base Case

Gold remains supported as:

Growth moderates

Real rates stabilize or decline

Geopolitical risks persist

Upside Scenario

An escalation in geopolitical tensions—particularly in energy markets—drives:

Higher inflation

Increased volatility

Stronger safe-haven demand

→ Gold outperforms

Downside Scenario

Sustained:

High real interest rates

Strong U.S. dollar

→ Limits upside and pressures gold prices

Investment Implications

Maintain a strategic allocation to gold as a portfolio hedge

Increase exposure in environments characterized by:

declining real interest rates

rising inflation expectations

heightened geopolitical risk

Monitor key indicators:

U.S. real yields (e.g., TIPS)

inflation trends

U.S. dollar strength

geopolitical developments

Conclusion

Gold’s dual role as both an investment asset and a central bank reserve asset reinforces its enduring importance in the global financial system.

As the economy transitions into a more fragile, late-cycle phase, the balance of risks—moderating growth, persistent inflation uncertainty, and elevated geopolitical tensions—appears increasingly supportive of gold.

From an investment perspective, gold provides:

Downside protection

Inflation resilience

Portfolio diversification

A disciplined allocation to gold can enhance portfolio resilience and serve as an effective hedge against evolving macroeconomic and financial risks.

Appendix:

Gold plays a dual role in global reserves—anchoring stability in advanced economies and hedging macroeconomic and currency risk in emerging markets. While advanced economies hold gold primarily for diversification and financial stability, countries facing higher inflation or currency volatility rely on it to preserve value and reduce reliance on major reserve currencies. Amid persistent currency fluctuations and macroeconomic uncertainty, gold remains a core reserve asset.

—

What Investors Are Asking About Gold Right Now

Why is gold performing well in 2026?

Gold prices are driven by four factors working together: real interest rates, inflation expectations, the strength of the U.S. dollar, and geopolitical risk. When real interest rates decline or stabilize, the cost of holding gold relative to interest-bearing assets falls, making gold more attractive. When inflation expectations rise, gold preserves purchasing power that bonds and cash cannot. In 2026, growth is moderating, inflation uncertainty has not resolved, and geopolitical tensions in energy markets remain elevated. That combination is historically supportive of gold, and it is reflected in current price behavior.

Should I increase my gold allocation if a recession is possible?

A recession is not the base case for 2026, but the conditions that precede one are increasingly in place. In that environment, gold serves a specific purpose: it provides downside protection when equity markets reprice risk, and it holds value when inflation prevents bonds from doing their typical defensive job. The case for increasing gold exposure is strongest when real interest rates are declining and geopolitical risks are elevated. Both conditions apply right now. The more relevant question for most investors is not whether to hold gold, but whether their current allocation is sized to actually matter if the scenarios that favor gold materialize.

What does central bank gold buying mean for individual investors?

Central banks, particularly in emerging markets, have been accumulating gold consistently over the past several years. They are doing so to reduce dependence on the U.S. dollar as a reserve currency and to strengthen their balance sheets against currency and inflation risk. For individual investors, sustained central bank demand creates a structural floor under gold prices that is independent of retail sentiment or short-term market moves. It also signals that the institutions with the most to lose from currency instability are treating gold as a core holding, not a speculative one. That is relevant context for any investor deciding how to think about their own allocation.

DISCLOSURE:

Fulcrum Wealth Advisors, LLC (FWA) is a registered investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). Registration with the SEC does not imply a certain level of skill or training. The firm is not registered as a broker-dealer and is not affiliated with any broker-dealer.

Additional information about FWA, including its services, fees, and business practices, is available in the firm’s Form ADV, which is available upon request or at www.adviserinfo.sec.gov.